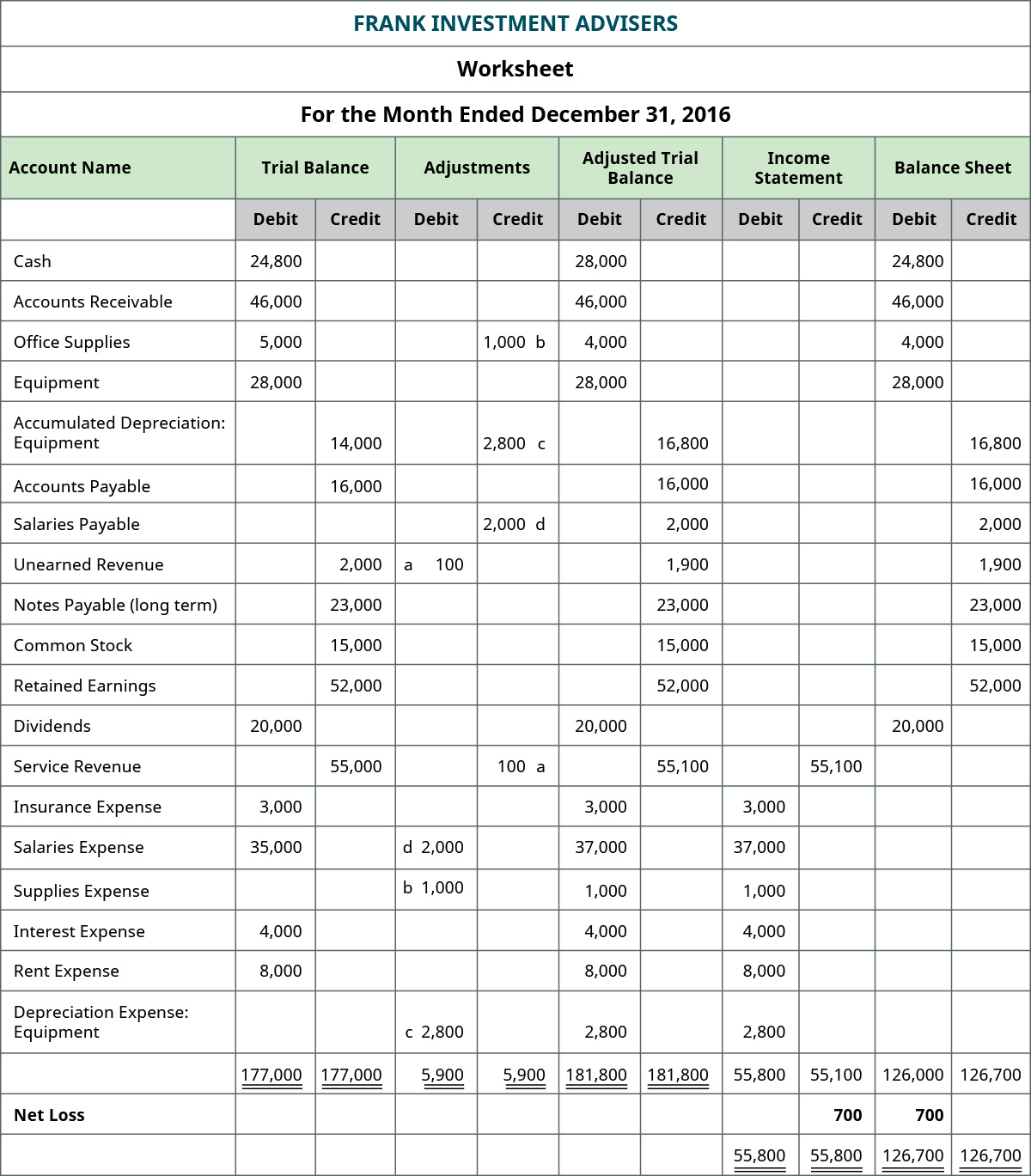

AccumulatedDepreciation–Equipment ($75), Salaries Payable ($1,500), UnearnedRevenue ($3,400), Service Revenue ($10,100), and Interest Revenue($140) all have credit final balances in their T-accounts. Thesecredit balances would transfer to the credit column on the adjustedtrial balance. The adjusted trial balance also helps identify discrepancies or errors that may have occurred during the initial recording of transactions. By reviewing the adjusted figures, accountants can detect and rectify inconsistencies, ensuring that the financial statements are free from material misstatements.

- There were no Depreciation Expense and Accumulated Depreciation in the unadjusted trial balance.

- Adjusted trial balance contains balances of revenues and expenses along with those of assets, liabilities and equities.

- Accrued revenues are revenues earned, but not received in monetary terms, and therefore represent receivables.

- By incorporating adjustments such as accrued revenues, expenses, depreciation, and prepaid expenses, the adjusted trial balance provides a more accurate representation of a company’s financial standing.

Adjusted Trial Balance vs Unadjusted Trial Balance

Deferred (unearned) revenues are revenues received that are included in liabilities until they are “earned”. Deferred revenue is “earned” upon delivery of goods or services to customers. The format of an adjusted trial balance is same as that of unadjusted trial balance. For example, if a company has earned interest income that hasn’t been recorded, you would make an adjusting entry to recognize this income. After incorporating the adjustments above, the adjusted trial balance would look like this.

First method – inclusion of adjusting entries into ledger accounts:

We are using the same posting accounts as we did for the unadjusted trial balance just adding on. Notice how we start with the unadjusted trial balance in each account and add any debits on the left and any credits on the right. In essence, the adjusted trial balance is a tool that confirms whether the ledger balances are accurate after accounting adjustments. Prepare the adjusted trial balance after the initial trial balance, which includes only the unadjusted balances of all accounts. The second method is simple and fast but is considered less systematic.

Effective Reconciliation for Accurate Financial Management

Most accounting software will let you generate a trial balance at any point in time to allow you to assess the current state of your accounts. The next step in the accounting cycle would be to complete the financial statements. Adjusted trial balance is a list of all the accounts of a business with their adjusted balances. Understanding how to prepare an adjusted trial balance maintains the integrity of financial data.

Reporting

Before the adjusted TB can be prepared, the year-end adjustments must be made. These adjustments usually include adjustments for prepaid and accrued expenses along with tax filing options 2021 non-cash expenses like depreciation. These adjustments are added to the unadjusted trial balance on the accounting worksheet and the new adjusted TB is prepared.

Latest blog posts

Once an adjusted trial balance is prepared, the company can prepare and issue financial statements and continue the process of closing its books at the end of the accounting cycle. For example, Interest Receivable is an adjusted account that hasa final balance of $140 on the debit side. This balance istransferred to the Interest Receivable account in the debit columnon the adjusted trial balance.

Following these steps will help ensure that your financial records are accurate and complete. Now that the trial balance is made, it can be posted to the accounting worksheet and the financial statements can be prepared. There’s also a chance it’ll fail to flag entries incorrectly coded to the wrong accounts, which can ultimately lead to inaccurate financial statements. A trial balance plays a major role in the accounting cycle, notably at the end of an accounting period before generating financial statements.

Within the trial balance, debit balances typically feature asset and expense accounts, while credit balances represent the company’s liabilities, capital, and revenue. Adjusting accounting transactions are recorded last in the transaction log and transferred to the General ledger, after which an Adjusted Trial Balance is compiled. The debits and credits might increase or decrease compared to the Unadjusted Trial Balance due to adjusting accounting entries, but the balance should still be maintained.

Such expenses might include paying for a rented space or any upcoming payments in the queue. Note that only active accounts that will appear on the financial statements must to be listed on the trial balance. If an account has a zero balance, there is no need to list it on the trial balance. Both ways are useful depending on the site of the company and chart of accounts being used. A trial balance only contains ending balances of your accounting accounts, while the general ledger has detailed transactions of the accounts. Notice the middle column lists the balance of the accounts with a debit balance, while the right column has balances for credits.

The adjusted trial balance (as well as the unadjusted trial balance) must have the total amount of the debit balances equal to the total amount of credit balances. After the adjusted trial balance is complete, we next preparethe company’s financial statements. Once the posting is complete and the new balances have been calculated, we prepare the adjusted trial balance. As before, the adjusted trial balance is a listing of all accounts with the ending balances and in this case it would be adjusted balances. Any difference indicates that there is accounting error in the journal entries or in the ledger or in the calculations.

Leave a comment